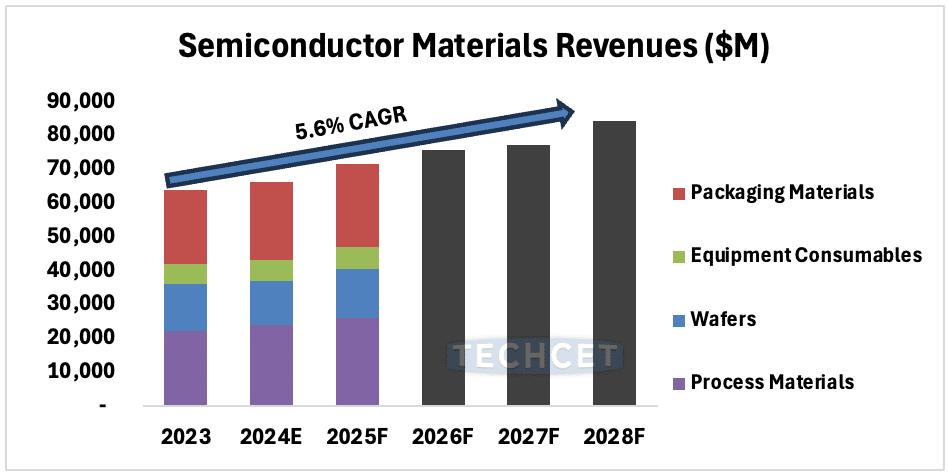

TECHCET — the electronic materials advisory firm providing semiconductor materials supply chain information — is anticipating growth of near 8% for the global semiconductor chip manufacturing materials market in 2025. AI-related device demand continues to push wafer starts upwards resulting in a 5.6% CAGR with total revenue exceeding $84 B USD by 2028.

In 2024, front end “Process Materials” led the recovery with an estimated revenue growth of nearly 7% over 2023 and an expected 7% CAGR through 2028. Among all process materials tracked by TECHCET, ALD/CVD, lithography materials, CMP ancillaries, and wafers are expected to have the strongest sequential revenue growth in 2025, each increasing more than 10%. Of note, the wafer segment revenue performance represents a strong rebound due to supply chain refresh, driven mostly by large diameter offerings.

The 2025 market is expected to be continually plagued with geopolitical tensions, particularly between the U.S. and China, with more export controls on technology, certain materials, and semiconductor manufacturing equipment. Nonetheless, semiconductor revenue growth is expected to be strong, driven by continued progress in AI and eventually aided by recovery in all markets, including broader compute, automotive, and mobile. Consumer electronics, PC segments, and automotive sectors are expected to have a slow start in 1H2025, with a stronger 2H2025, pushing overall materials revenues up in the 8% to 10% range for the year.