IC Insights released its June Update to the 2020 McClean Report earlier this month. This Update included a 2018-2024 IC database that segmented the IC market by major product type including Consumer, Auto, Computer, Industrial, Communications, and Government/Military end-use applications in the Americas, Europe, Japan, China, and Asia-Pacific regions.

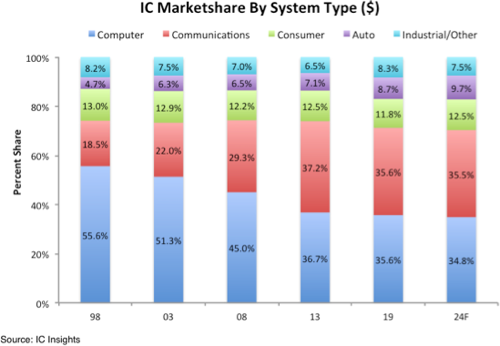

Over the past 21 years, the communications IC segment almost doubled its share of the total IC market from 18.5% in 1998 to 35.6% in 2019 (Figure 1).

Communications overtook the computer segment as the largest end-use market for ICs in 2013 but was passed by the computer segment in 2017 and 2018 because of the booming memory market (since more memory is used in the average computer than in the average communication system). However, with the deep plunge in the 2019 memory market, communications and computer tied for IC marketshare in 2019, but the communications segment is expected to edge ahead of all other end-use applications by 2024.

As shown, the automotive IC marketshare has displayed a steady increase since 1998 going from a 4.7% share that year to 8.7% in 2019. Moreover, the automotive market is forecast to register the strongest 2019-2024 CAGR of any of the end-use segments at 9.7%. Unfortunately, given its relatively small size, high growth in the automotive IC segment is not expected to be enough to significantly lift the growth rate of the total IC industry over the next five years.

In contrast to the expected rising shares of the automotive and consumer segments through 2024, the computer and industrial/other IC marketshares are forecast to drift lower over the next five years. The computer segment’s share of the total IC market dropped 20 points since 1998 to 35.6% in 2019. However, strong server demand to help support the Internet of Things is expected to pump new life into the computer IC market over the next five years and slow the rate of marketshare decline for this segment.

One thing to keep in mind with regard to IC end-use marketshare figures is that they typically move at an evolutionary, not revolutionary, pace. Major changes and trends in the end-use percentage figures are sometimes only evident when looking at five or ten year timeperiods. Overall, this is one aspect of the IC industry that requires some perspective that only relatively long periods of time can provide.