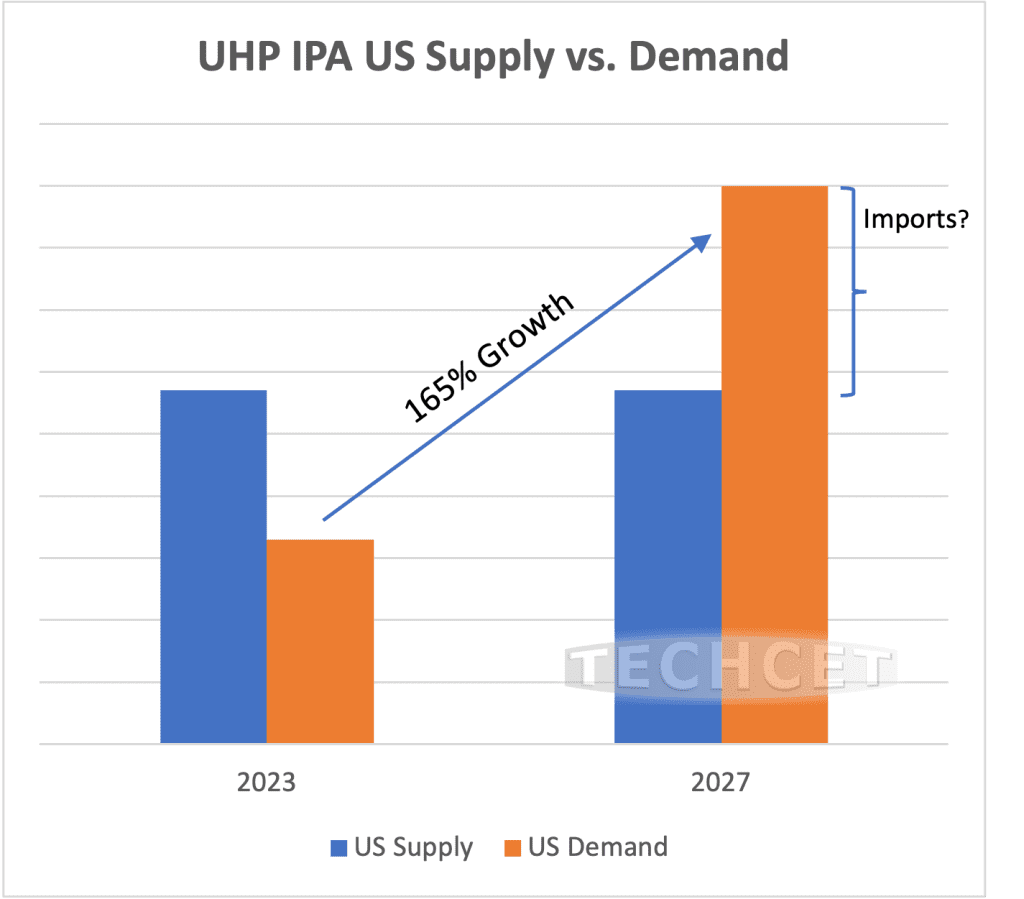

TECHCET—the electronic materials advisory firm providing market and supply-chain information — is forecasting a jump in the US domestic share of the semiconductor material market to 13-15% by 2027, as support grows for incoming fab expansions. While this outlook is looking generally positive for the US semiconductor industry, uncertainties with timing expansions have made it difficult for suppliers to plan effectively and CHIPS Act funding does not seem to be helping. In many cases, suppliers are “expansion-ready,” and are just awaiting demand signals from chip manufacturers. As a result, much of the incremental US wet chemical capacity is focused on an “import first, build later” strategy, meaning capacity is being used to warehouse, possibly purify, repackage, and distribute imported chemicals, rather than manufacture them domestically. This is the case in regard to IPA, as shown in the graph below. Although the potential growth is high, the timing is uncertain.

While this import-focused approach helps meet initial fab needs, it keeps the US chip industry dependent on exports, which can bring instability to the supply chain. As wafer start capacity grows, this dependence on exports will grow in parallel, unless suppliers are able to ramp capacity accordingly, as shown in TECHCET’s new market report on the “Impact of Chip Expansions on the US Wet Chemicals Supply Chain.”

Asia-based suppliers such as AUECC, ENF, and MGC among others, have established and/or are expanding US operations to support the domestic chip manufacturing expansion. In addition, some US-based suppliers (PVS, Entegris, etc.) have initiated or announced plans to increase capacity for semiconductor wet chemicals. Timing uncertainties have remained an issue though, as many of the partnership activities, such as with Kanto and Chemtrade, have been stopping and starting with fab announcements.

Suppliers are currently concerned that the US CHIPS and Science Act is not supporting the full supply chain as originally hoped. Fabs and equipment manufacturers remain the priority of CHIPS Act funding. Material suppliers see the Notice of Funding Opportunity (NOFO) as offering little support without tax incentives, and are unclear what funding will be leftover for them. Furthermore, the NOFO discourages small projects stating that projects under $20M are unlikely to be approved.