The COVID-19 pandemic is wreaking havoc on sales of automotive power semiconductors, with falling demand for motor vehicles causing global market revenue to decline by 16 percent in 2020.

Worldwide revenue for power semiconductors used in automotive applications will fall to $9.1 billion in 2020, down from $10.8 billion in 2019, according to Omdia’s Power Semiconductors in Automotive Report – 2020.

“The year 2020 had been expected to bring a rebound for the automotive power semiconductor market,” said Kevin Anderson, practice lead for power, automotive and industrial semiconductors for Omdia. “However, the COVID-19 pandemic shut down most automotive assembly plants for several weeks—first in China and then throughout the rest of the world. At the same time, demand for new vehicles has fallen as dealerships were closed and lost jobs and wage reductions in many parts of the world combined to slash demand.”

Even those plants that have reopened are not all operating at full capacity, due to component shortages and reductions in the numbers of employees on production lines as physical distancing measures are implemented. As a result, current new-vehicle build forecasts envision production of less than 70 million units in 2020, a decline of more than 20 percent from 2019.

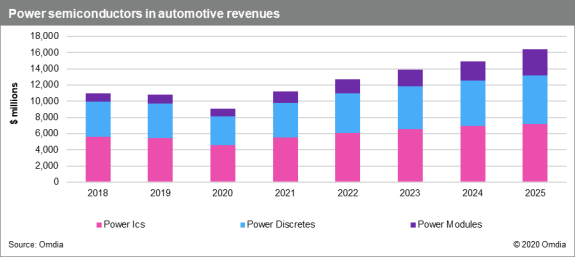

Power semiconductor devices, including power discretes, power modules and power integrated circuits (ICs), are used extensively throughout automotive electronics systems. This widespread adoption has propelled strong annual growth in the high-single-digit percentages for the automotive power semiconductor market in recent years.

However, 2019 brought a reversal in that trend. Trade tensions throughout the year combined with on-and-off tariff negotiations and the decline in some regional economies reduced vehicle builds and caused the automotive power semiconductor market to decline 1 percent compared to 2018.

Automotive power semis shift into reverse

After experiencing declines in the low single digits in 2019, discrete power semiconductors and power ICs for automotive applications are expected to post sharp revenue losses of 17 percent during the current year. These devices are used throughout vehicle electronic systems, and because the electronic content and the complexity of those systems is increasing, the impact of reduced vehicle production on their revenue has been limited.

Power module revenues grew by 7 percent in 2019, benefitting from the increased manufacturing volumes of electric vehicles (EVs) and hybrid EVs (HEVs). Similarly, only an 8 percent decline in power module revenue is forecast for 2020.

The revenue outlook for various automotive domains is also mixed.

Revenue from the fast-growing advanced driver assistance systems (ADAS) module market posted a 12 percent increase in 2019 and is expected to fall by only 3 percent in 2020. In powertrain systems, revenue grew by 1 percent in 2019 and is forecast to decline by 13 percent in 2020. Sales of higher-value power modules are expected to rise due to the automotive market’s conversion to HEV/EV production. The other domains—body and convenience, chassis and safety and infotainment—grew in the mid-single digits in 2019 and are expected to decline by a high-teens to low-20s percentage in 2020.

Recovery takes the driver’s seat for 2021

As the major world economies seek to reopen after lockdown, a gradual pickup in sales is expected in the second half of 2020. If a serious second wave of the virus can be avoided and a COVID-19 vaccine or improved treatments can be developed by early 2021, then a rebound of vehicle sales is envisioned for 2021.

This would result in an increase in power semiconductor sales close to the mid-20-percent range in 2021. Furthermore, the long-term compound annual growth rate (CAGR) would return to 7 percent for the years 2019-2025.

The Omdia Power Semiconductors in Automotive Report -2020 presents a much deeper analysis of the market, including breakouts by 35 electronic application areas and 30 different semiconductor device types.