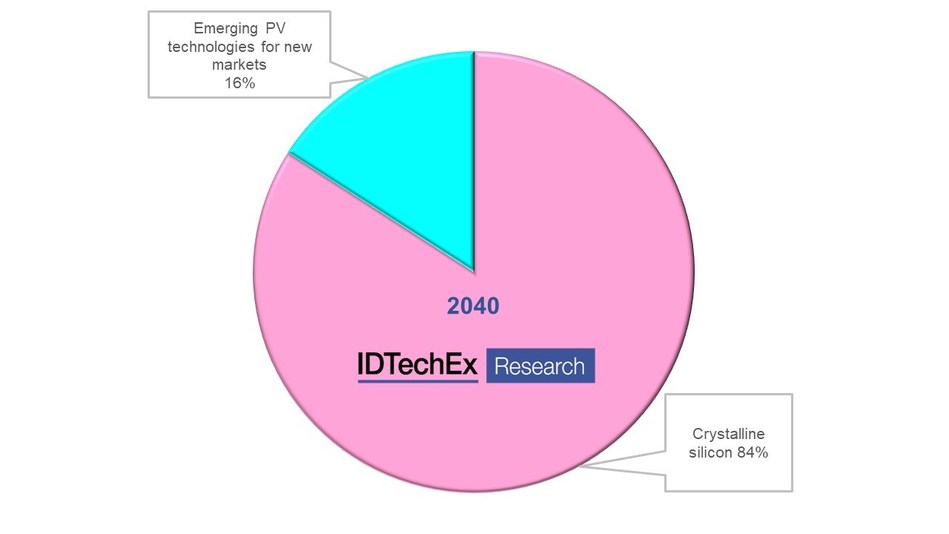

The new IDTechEx report, “Materials Opportunities in Emerging Photovoltaics 2020-2040,” is based on interviews by multi-lingual, PhD level IDTechEx analysts across the world and 20 years tracking the research and applications. They predict $38 billion dollars in 2040 without colliding with the silicon-in-glass “power station” business. There will be many opportunities for premium pricing of its new specialist materials.

For example, over $10,000/W is currently paid for record 30% efficient lll-V compound PV in a designer watch, as an array on a satellite or surface of a high-altitude drone. Another emerging PV technology copper-indium-gallium-diselenide PV has recently shot to over $2 billion sales in only ten years. Most of the emerging PV is thin film, flexible and some will be stretchable, creating many new markets. Tightly-rollable PV in your mobile phone, regular aircraft skin, billions of Internet of Things nodes?

Hundreds of millions more building facades need this lightweight PV. Tripled-efficiency indoor “lll-V” PV is newly on sale to be followed by underwater. Researchers even target three technologies for PV paint. Vehicle retrofit from boats to buses… this list goes on and on. (Those interested in radically new formats for electronics and electrics in general, should see the IDTechEx report, “Electronics Reshaped 2020-2040“).

Excitingly, the PV research pipeline guarantees robust further improvements to the already dramatic leap in life, efficiency, cost and so on in recent years. CIGS will join organic photovoltaics OPV in being totally free of heavy metals that could be emitted during abuse or wrongful disposal. Rare materials subject to price hikes are being bypassed. Transparency, biodegradability, availability of wide area film, layering different technologies on top of each other – all open up more sales.

Whisper it quietly, but with silicon near its theoretical limits and taking massive areas of real estate – often prime agricultural land and lakes – that multijunction, compound-semiconductor PV being developed by Toyota on a car may possibility even compete with “power station” silicon one day by affordably providing the power in half the area and therefore being much more widely deployable and acceptable.

The 200 page IDTechEx report, “Materials Opportunities in Emerging Photovoltaics,” starts with an executive summary and conclusions sufficient for those with limited time. Here 18 primary conclusions, 2020-2040 forecasts and roadmaps by technology, the price sensitivity and learning curves projected forward, gaps in the market, the application hierarchy and a contrast with the totally different silicon business with its price war and fight to the death in China. The introduction then reveals the amazing virtuosity of PV already, important parameters, SOFT report, PV architectures, efficiency trends. In particular, see the primary PV options beyond silicon compared in detail, including production readiness and 13 examples of new formats, progress to user customisation and many new locations and combinations.

Chapter 3 dives into inorganic compound semiconductor lll-V PV architectures, material opportunities backed by Boeing Spectrolab, Lightricity, Toyota and others and the cost reduction routes to volume sales researched by NREL. Chapter 4 concerns copper indium gallium diselenide CIGS opportunities including laboratory progress in cost reduction, efficiency increase and elimination of cadmium with new architectures. See activities of Ascent Solar, Flisom-EMPA, Manz, Renovagen, Solar Frontier and others. Chapter 5 on organic OPV materials opportunities reveals its recently-transformed competitive situation and future with rapid efficiency and life increase, profiling many players including Armor-Opvius, Heliatek, materials suppliers and gaps in the market. New molecule choices, fullerene elimination and its critical barrier layers are here.

Chapter 6 is a sober look at the now-fashionable perovskite PV balancing stellar efficiency gains with challenges in stability and use of lead and what is being done about it. Chapter 7 wraps up the basic chemistry options with dual technology such as perovskite on silicon or CIGS then quantum dot and wild card PV opportunities. Here are toxicity issues, rectenna harvesting and 2D materials. Chapter 8 and 9 are a close analysis of the important conductive pastes and barrier layers used overall.

Only the IDTechEx report, “Materials Opportunities in Emerging Photovoltaics 2020-2040” presents new, global, facts-based analysis of materials in emerging photovoltaics on a 20 year view. For the whole harvesting industry see the IDTechEx report, “Energy Harvesting Microwatt to Gigawatt: Opportunities 2020-2040.”

For more information on this report, please visit www.IDTechEx.com/MaterialsPV or for the full portfolio of research available from IDTechEx please visit www.IDTechEx.com/Research.