Today’s chip shortage has put a spotlight on the degree to which the European economy depends on semiconductors. With limited local production capability and capacity, Europe risks its technological sovereignty and needs to correct course to maintain long-term competitiveness.

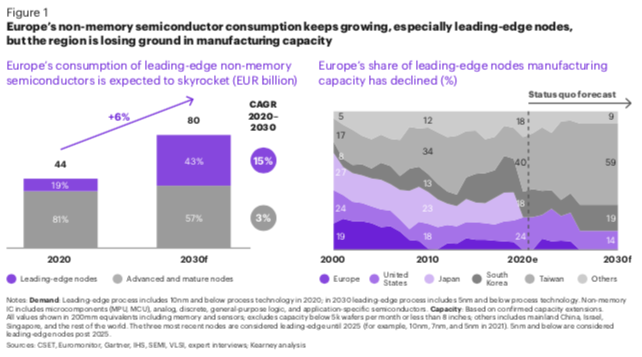

As digitalization transforms more and more aspects of our lives, consumption of leading-edge semiconductors will almost double the EU’s total consumption by 2030 at an annual growth rate of 15 percent, while demand for mature semiconductor technologies will grow more modestly with a CAGR of 3 percent (see Figure 1).

In 2000, Europe was a leading producer of semi- conductors and home to almost 25 percent of the world’s manufacturing capacity. Today, output has dropped to 8 percent. An even more drastic decline occurred in leading-edge semiconductor technology, with market share dropping from 19 percent in 2000 to zero today (see Figure 1).

The EU has set a strategic ambition to more than double its share of semiconductor manufacturing to 20 percent by 2030. Although there is general agreement on the need to strengthen the EU’s positioning in the semiconductor industry, discord regarding the right strategy to achieve this goal divides European political and business leaders.

Europe would significantly benefit from local leading-edge chip manufacturing and is well positioned to succeed

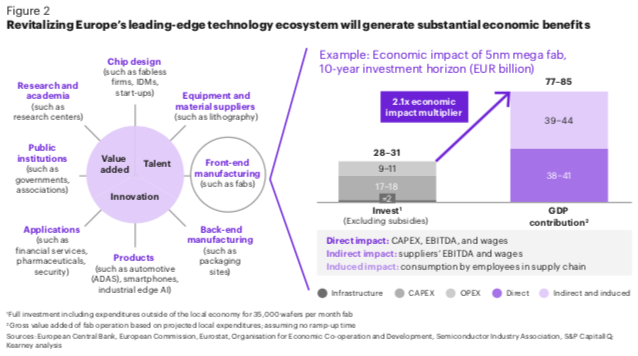

Success at the forefront of semiconductor technology relies on a combination of advanced engineering (research and design) and manufacturing (equipment and fabrication) capabilities. Integrating these domains has been a historical strength of Europe, for instance in the automotive industry. Europe holds strategic assets in the semiconductor value chain. Backed by leaders in fab equipment, top R&D capabilities and engineering talent, a stable political environment, excellent infrastructure, and the necessary financial muscle, Europe has what it takes to reestablish the region’s competitiveness in leading-edge semiconductor technology.

Strengthening leading-edge semiconductor technology can bring Europe significant economic benefits. A leading-edge semiconductor manufac- turing fab creates more than two times the initial investment in economic impact (see Figure 2).

It would also give rise to new business opportunities and provide a breeding ground for local start-ups. Furthermore, chip manufacturing in Europe would bolster the region’s technological sovereignty and improve supply chain resilience.

European fab operations currently suffer from total cost of ownership disadvantages against other regions. Over 10 years, operating a new leading-edge fab in Europe is 30 percent more expensive compared with South Korea and more than 40 percent when compared with Taiwan. The main differences are the regional incentives, co-investments, and subsidies. Unless it changes the status quo, Europe will lose even more of its global position.

Pulling European semiconductor manufacturing into the fast lane

Investments in semiconductor technology are very high and increasing for leading-edge technology in engineering and manufacturing. We believe two parallel efforts are required to make progress against the EU’s strategic ambition in the next 10 years.

First, reinvigorate the local semiconductor ecosystem. This can be achieved by incentivizing leading-edge chip design, manufacturing capacity, including fabs and ATP sites, and fundamental research. These activities would spur additional developments in mature technology and scale into the remaining parts of the ecosystem.

Second, partner with leading-edge semiconductor technology companies. As Intel, Samsung, and TSMC pledged to invest more than EUR 300 billion by 2030, a unique window of opportunity opens up that would allow for combining the EU’s strengths with the partners’ expertise and de-risk the realization of its ambitions.

With 2030 just around the corner, now is the time for Europe to decide its destiny in semiconductors.