PIERRE CAMBOU, MSc, MBA, is Principal Analyst, Global Semiconductors at Yole Group.

In 2023 for the first time in a 50-year long history European semiconductor companies have reached 14% market share, departing from the mere 9% to 11% it had in the last decades. Many had laughed at the 20% market share goal set by Thierry Breton who just resigned from the commissioner position. Considering those recent numbers this was not unreachable after all. There is a little bit of Mark Twain in this situation “they did it because they didn’t know it was impossible”.

While European device companies sell chips and are part of a $530B market, the key question of securing supply chains has come to the forefront. In the wake of COVID-19 semiconductor shortages combined with geopolitical tensions had regulators in the US and EU sign up for massive CHIP-ACT subsidies to the combined amount of $100B. The goal is to “re-shore” semiconductor production with state-of-the-art foundries on both side of the Atlantic instead of relying – too much – on Asian supplies.

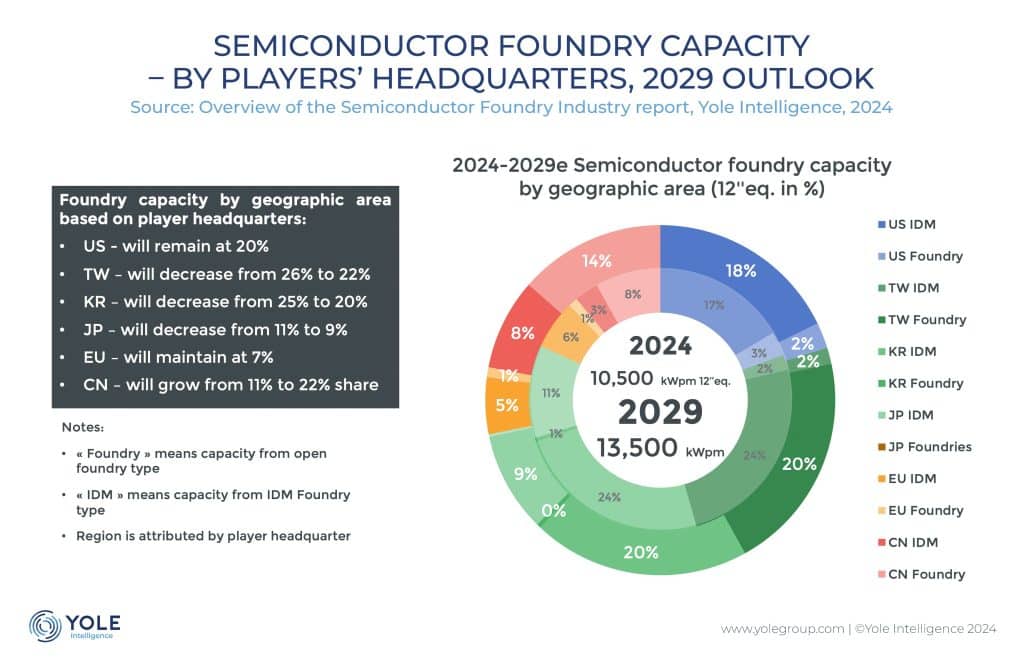

Doing the math of all announces around the world Yole has come-up with a picture (Overview of semiconductor foundry 2024) of the possible outcome in 2029. It is one thing to announce the construction of a “fab”, yet another to ramp-up production, put yields under control, and output 25k wafers per month as the most modern 300mm foundries do. The recent push back of at least 2 years of Intel’s Magdeburg Fab is a reminder that words are cheap and actions expensive, especially when it come to semiconductor foundries. In 2024 Europe control 7% of the world foundry capacity which means it must process 50% of its wafers elsewhere either by foundry ownership abroad or purchases to an open foundry such as TSMC, or Samsung Semiconductor.

So far European foundry capacity is expected to grow 20% by 2029, just enough to maintain the current capacity share. What is new is the effort from foreign players INTEL and TSMC outpacing the locals, Infineon Technologies, ST Microelectronics and Bosch who will only grow by 5%.

This is indeed matching the expected wafer demand growth at world level. European players are playing carefully and for good reasons. As of October 2024, they are suffering the recession, others have experienced a year ago. On their markets, automotive and industrial semiconductors, prices have gone down and so the fear of shortages, reducing stockpiling and thus orders.

These markets will start to grow again next year. Europe will be ready to grow again its market share but should maintain the current status quo and still source about 50% of production abroad. Maybe a little more from the U.S., if foundry constructions get more successful over there. But was it not the goal after all?