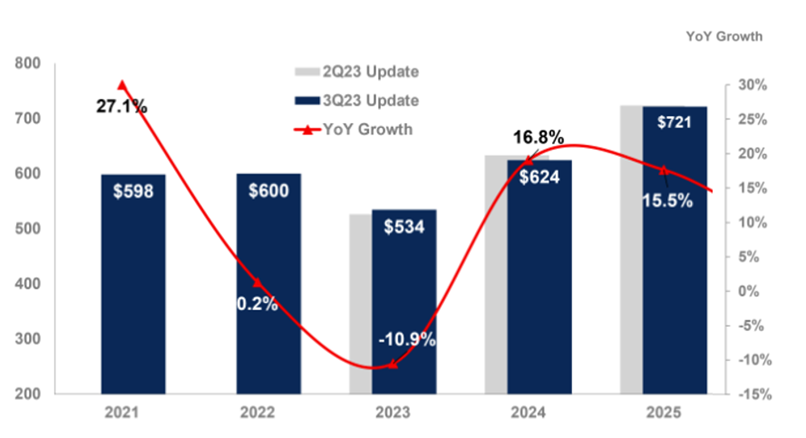

Global semiconductor revenue is projected to grow 16.8% in 2024 to total $624 billion, according to the latest forecast from Gartner, Inc. In 2023, the market is forecast to decline 10.9% and reach $534 billion.

“We are at the end of 2023 and strong demand for chips to support artificial intelligence (AI) workloads, such as graphics processing units (GPUs), is not going to be enough to save the semiconductor industry from double-digit decline in 2023,” said Alan Priestley, VP Analyst at Gartner. “Reduced demand from smartphones and PC customers coupled with weakness in data center/hyperscaler spending are influencing the decline in revenue this year.”

However, 2024 is forecast to be a bounce-back year where revenue for all chip types will grow (see Figure 1), driven by double-digit growth in the memory market.

Memory Revenue to Rebound in 2024 After Double-Digit Decline

The worldwide memory market is forecast to record a 38.8% decline in 2023 and will rebound in 2024 by growing 66.3%.

Anemic demand and declining pricing due to massive oversupply will lead NAND flash revenue to decline 38.8% and fall to $35.4 billion in revenue in 2023. Over the next 3-6 months, NAND industry pricing will hit bottom, and conditions will improve for vendors. Gartner analysts forecast a robust recovery in 2024, with revenue growing to $53 billion, up 49.6% year-over-year.

Due to high oversupply level and lack of demand, DRAM vendors are chasing the market price down to reduce inventory. Through the fourth quarter of 2023, DRAM market’s oversupply will continue which will trigger a pricing rebound. However, the full effect of pricing increases will only be seen in 2024, when DRAM revenue is expected to increase 88% to total $87.4 billion.

Integrating AI Techniques Will Generate New Servers

Developments in generative AI (GenAI) and large language models are driving demand for deployment of high-performance GPU-based servers and accelerator cards in data centers. This is creating a need for workload accelerators to be deployed in data center servers to support both training and inference of AI workloads. Gartner analysts estimate that by 2027, the integration of AI techniques into data center applications will result in more than 20% of new servers including workload accelerators.

Gartner clients can read more in “Forecast Analysis: Semiconductors and Electronics, Worldwide” and “Semiconductors and Electronics Forecast, 3Q23 Update, Presentation Materials.”