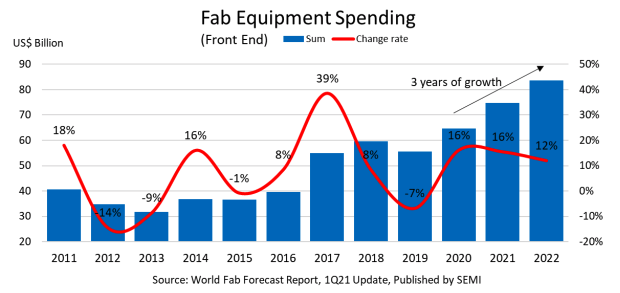

Fueled by surging pandemic-inspired demand for electronics devices, the global semiconductor industry is on track to register a rare three consecutive years of record highs in fab equipment spending with a 16% increase in 2020 followed by forecast gains of 15.5% this year and 12% in 2022, SEMI highlighted today in its quarterly World Fab Forecast report.

Fabs worldwide will add about $10 billion worth of equipment in each of the three years as spending climbs to top $80 billion at the end of the forecast period. Explosive demand for electronics that are the backbone of communications, computing, healthcare and online services – sectors that mounted robust responses to the COVID-19 outbreak as the world rallied to curb the coronavirus’s spread – account for much of the spending.

Fab equipment spending has historically been cyclical, with one or two years of growth typically followed by a downtrend of roughly equal length. The semiconductor industry last saw three straight years of fab equipment investment growth in a run that started in 2016. It was nearly 20 years before that streak that the industry recorded an expansion of at least three years. In the mid-1990s, the chip industry boasted a four-year period of growth.

The bulk of fab investments in 2021 and 2022 will be seen in the foundry and the memory sectors. Driven by leading edge investment, foundry spending is expected to grow 23% in 2021, reach $32 billion and flatten in 2022. Overall memory spending will increase in the single digits to reach $28 billion in 2021 while DRAM will surpass NAND Flash, and then surge by 26% in 2022 on the strength of both DRAM and 3D NAND investment.

The power and MPU segment will also see strong spending growth over the forecast period. Power is forecast to show strong investment growth of 46% and 26%, respectively, in 2021 and 2022 driven by strong demand for power semiconductor devices. MPU will add to the momentum with 40% growth in 2022 as microprocessor investments increase.

The World Fab Forecast report lists 1,374 facilities and lines globally, including 100 future facilities and lines with various probabilities that will start volume production in 2021 or later.