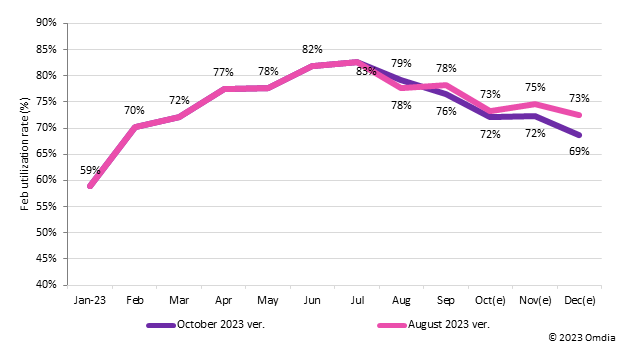

As demand and panel makers’ efforts on LCD panel price protection slows down, display fabs’ overall utilization are expected to drop below 70% in 4Q23, according to Omdia’s latest Display Production & Inventory Tracker.

Display panel makers’ monthly fab utilization latest forecast

“Panel makers continued to increase LCD TV display price in 3Q23 which brought strong panel price pressure from TV brands/OEMs. As LCD TV display buyers started to cut panel purchasing from 3Q23 panel makers began reducing their fab utilization and the so-called production-to-order policy”, said Alex Kang, Principal Analyst in Omdia’s Display practice.

“Following the LCD TV display price pressure from TV brands/OEMs, panel buyers are realizing they will need to modify their purchasing plans over the coming months including in 1Q24 if meaningful reductions in LCD TV panel prices are not applied. Compared to a couple of months ago, panel makers have cut their fab utilization more aggressively in the latest forecast which implies panel makers are struggling to sustain LCD TV panel prices,” added Kang.

This LCD TV display supply/demand trend is set to cause difficulties for panel makers during 4Q23 – 1Q24. Several TV brands are suffering the impact of increased TV inventories from 3Q23 due to slower demand while other TV brands are suffering from poor profits as a result of LCD TV display price hike from 3Q23. These factors combined are pushing panel makers to lower panel prices significantly.

Subsequently, panel makers particularly Chinese panel makers are considering dropping fab utilization significantly in 1Q24 to approximately below 60%. This drop is expected around the Chinese New Year holiday season in February 2024 with a hope to ultimately minimize panel price erosion in 1Q23.

Meanwhile, panel makers fab utilization cut trend is not only expected for LCD TV displays but also for IT LCD such as notebooks, PCs and monitors. PC brands and OEMs are cautious to buy IT LCDs to avoid carrying over inventory to the next year. IT LCD buyers want to see 2023 year-end shopping season results first before making any purchasing decisions.

Although PC brands and OEMs expect commercial demand from the B2B market in 2024, their hope for this demand is lessening due to the forecasted global recession. The inevitable slower IT LCD demand till early of 2024 may bring deeper utilization cut in 1Q24 concludes Omdia.