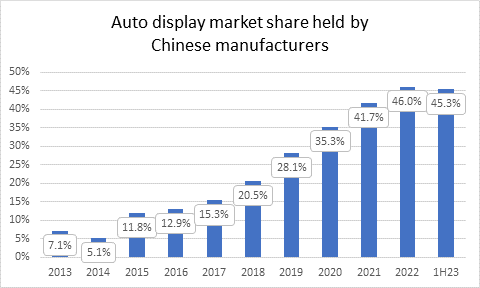

Chinese companies have emerged as the top suppliers in the automotive display market in the first half of 2023, extending their dominance in the displays industry after also dominating the TV and smartphone display markets. According to Omdia’s Automotive Display Intelligence Service, Chinese companies hold 45.3% of the market share, a significant increase from their 7.1% share a decade ago. Additionally, Chinese suppliers now retain a majority share of 55.5% in the a-Si LCD market and have entered the OLED market with a 17.8% share.

BOE and Tianma are the two major contributors to this growth, with their combined share reaching 30.7%. BOE stands out as the only panel supplier with a market share of over 15%. The company has ample capacity to meet the demands of the automotive display market, with two Gen8.6 TFT LCD fabs (one a-Si, the other Oxide) and two Gen6 OLED fabs that offer affordable platform models. BOE has established itself as the center stack display and aftermarket leader. Meanwhile, Tianma continues to expand its production line capacity for automotive displays, with a-Si LCD being its primary application. In addition, Tianma dominates the instrument cluster display market with a lion’s share of 24%.

“Omdia expects the Chinese suppliers to maintain a high level of capacity for automotive display production,” said Stacy Wu, Senior Principal Analyst at Omdia’s Displays practice. “In addition to BOE, HKC, Tianma, and CSOT have also planned to allocate a certain amount of Gen8.x a-Si/Oxide LCD for automotive use. BOE and Tianma are set to shift more LTPS LCD capacity from smartphone display to automotive after CSOT. On top of BOE and EDO, Tianma, CSOT, and Visionox are also planning to manufacture OLED automotive displays. The Chinese players’ strength in cost and capacity will continue to give them an advantage in dominating the automotive display market.”