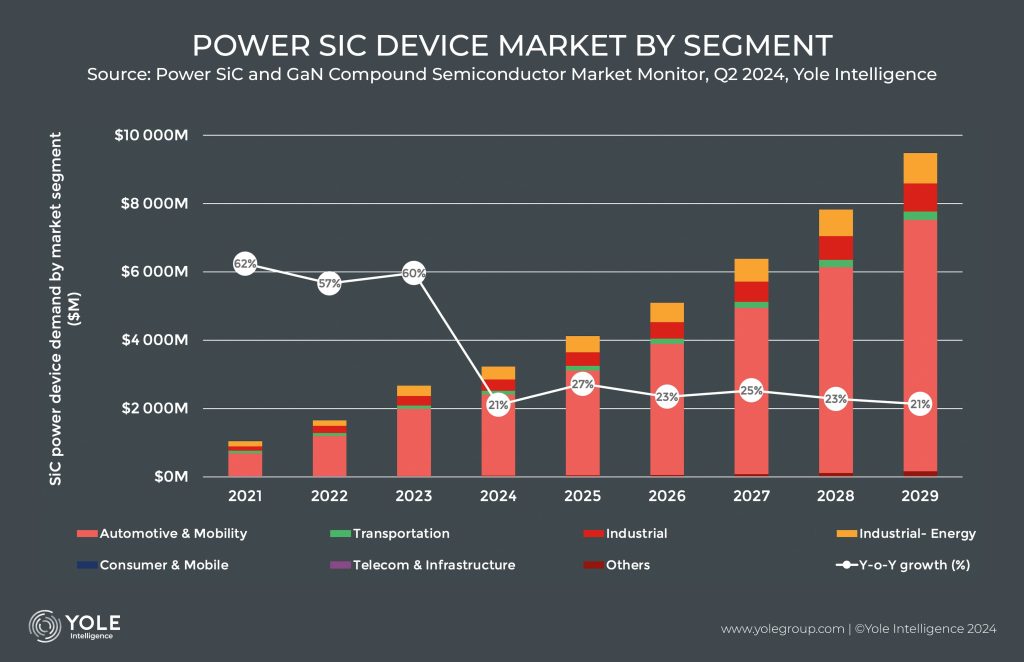

The power SiC market has surged since Tesla adopted SiC MOSFETs in its inverters in 2017. As of 2024, high-volume SiC based EVs, including models from Tesla, BYD, and Hyundai, are using SiC MOSFETs in traction inverters. Beyond automotive, sectors like industrial, energy, and rail are also driving growth. The SiC devices market is expected to reach nearly $10 billion by 2029, with SiC wafer and epiwafer shipments growing to over 3 million units.

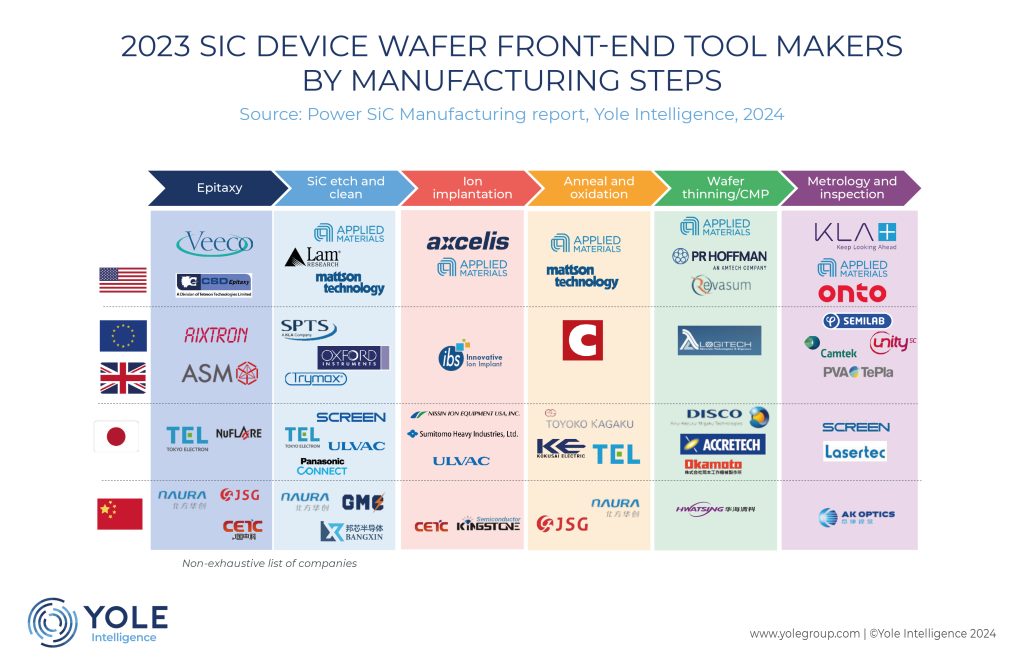

This booming market is attracting significant investment and capacity expansion across all levels, from devices to wafers. Leading players are expanding facilities, boosting equipment orders. The dynamics and forecast of the SiC manufacturing tool market are detailed in Yole Group’s new Power SiC – Manufacturing report. It highlights the need for dedicated WFE tools for processing power SiC devices, focusing on critical steps like epitaxy tools, ion implantation, wafer thinning, dry etching, annealing, oxidation, and inspection and metrology (M&I).

SiC epitaxy by HTCVD, crucial for device performance, saw equipment billing double to $555 million in 2023, with cumulative revenue projected to reach $4.8 billion by 2029. The ion implanter market is expected to generate $5.4 billion over the same period. Annealing and thermal oxidation equipment are forecasted to contribute nearly $1.4 billion.

M&I for SiC processing, essential for detecting surface and subsurface defects, is expected to reach $7 billion in cumulative revenue by 2029. Other growing tools include burn-in test, patterning, wafer bonders, thinning, and CMP.

The overall WFE SiC manufacturing tool market is projected to grow at a 6.5% CAGR from 2023 to 2029, reaching $4.4 billion by 2029, peaking in 2026, followed by a gradual decline. WFE revenue aligns with CapEx trends, maintaining 50-60% ratio annually, according to Yole Group.

Supply chain overview: tool makers keeping the pace with SiC evolution with concerns on over-capacity

Due to the growing SiC device market, players are investing heavily. In 2023, global CapEx in the power SiC sector is estimated at $4.4-5.6 billion, nearly double the SiC device market’s $2.7 billion. This CapEx is expected to peak in 2026 as capacity buildouts conclude. In the meantime, many device manufacturers plan to start the production in their 8” lines. To have the production lines opened in the next 2 year time, the investments start now, but many process challenges have to be still resolved.

China becomes a major player in the Power SiC market, capturing over a third of the SiC wafer and epiwafer market in 2023. Despite having active PVT and HTCVD players, China’s equipment supply is not yet self-sufficient at all levels, delaying its device players’ market share growth.

Regarding now market shares. Many leading SiC chipmakers develop their own PVT tools in-house to control quality. The open PVT market is led by Chinese suppliers like NAURA and CGEE, with European and Korean competitors following. The HTCVD tool market is dominated by Aixtron, with new Chinese entrants like NAURA and Naso Tech rapidly growing due to increased demand for epiwafer capacity. The WFE tool landscape varies by step. The SiC ion implanter market is dominated by Axcelis, with other companies adapting Si processing equipment for SiC, such as ULVAC and Applied Materials. Players from the photovoltaic industry, like CETC and Kingstone from China and Nissin Ion from Japan, are also entering the SiC processing market.