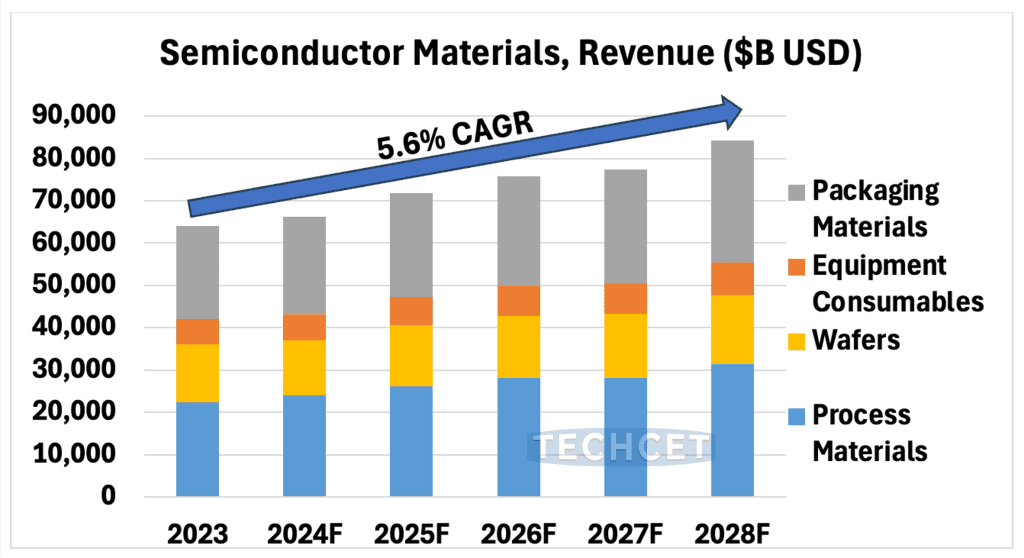

TECHCET— the electronic materials advisory firm providing semiconductor materials supply chain information — is forecasting a rebound in the global semiconductor chip manufacturing materials market in 2024. Following a 12% year-over-year decline in 2023 driven by a sluggish industry and inventory correction, revenues for total materials in 2024 is expected to see 3-4% growth as conditions improve.

The 2024 market has been plagued with geopolitical tensions, particularly between the U.S. and China, with stricter export controls on technology, certain materials, and semiconductor manufacturing equipment. Despite these and other global tensions, the semiconductor market shows signs of mixed recovery from the downturn of 2023, driven by a boom in AI-related demand and data center build outs. Fortunately, any excess chip inventory has been winding down and demand is stabilizing. However, consumer electronics, PC segments, and automotive sectors continue to struggle, keeping overall market growth to modest levels.