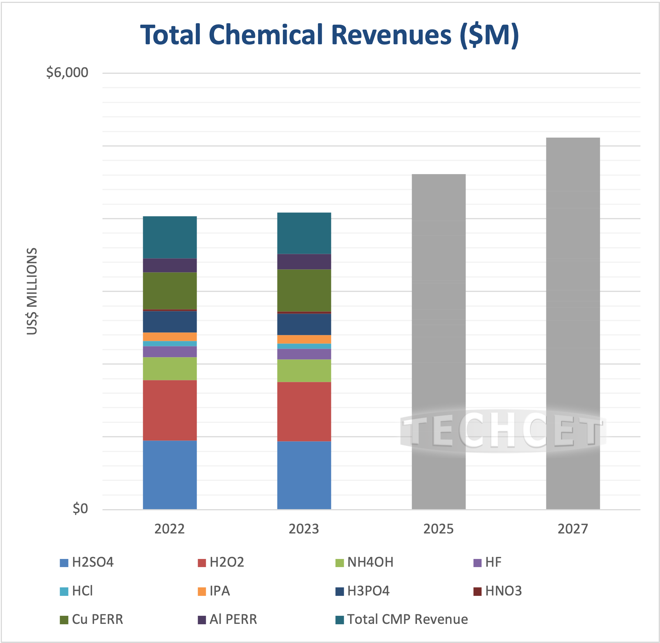

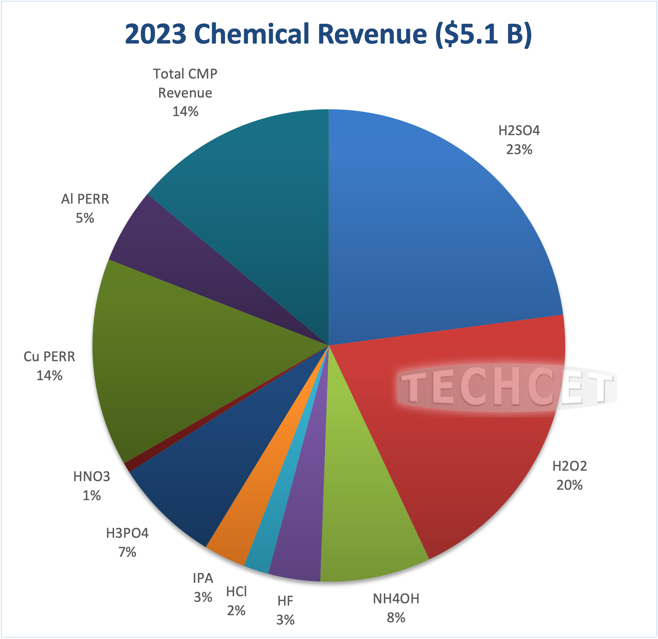

TECHCET— the electronic materials advisory firm providing business and technology information on semiconductor supply chains — is forecasting 2023 semiconductor wet chemical revenues to hit $5.2B, a 2% decrease from 2022. This forecast follows wafer start trends, which are also expected to decline by about 3% in 2023. The slowdown is also attributable to rising energy prices and instability from the Russia-Ukraine war, as highlighted in TECHCET’s newly published Wet Chemicals Critical Materials Report. The strongest of the wet chemicals segments is from phosphoric acid, due to growth in the 3DNAND market. The overall market is forecasted to rebound in 2024, with the 2022-2027 CAGR being 3.9%, as shown in the graph below.

“2023 is teaching us that a holistic approach to the chemical supply chain is required to stay competitive,” states Dan Tracy, Sr. Director at TECHCET. Tracy added, “to be successful in the wet chemicals market, one must be actively involved in all stages of the supply chain.” For example, shortages due to refinery shutdowns affects the cost and availability of multiple chemicals such as IPA and sulfuric acid. Additionally, shortages of fluorspar affect the availability and cost of HF and BOE.

Chemical price increases have occurred due to higher pricing and restrictions of natural gas and petroleum used for power in chemical manufacturing. For example, costs of European electronic chemicals have increased due to rises in the cost of natural gas. Although these natural gas costs have come down from its highs of 2022, chemical prices still remain higher than before the Russia war. Similar trends have been observed in other chemical manufacturing regions over the past two years.